We assist in GST Adjudication and Appeal proceedings.

Appeal to First Appellate Authority, Appeal to GSTAT (Goods and Services Tax Appellate Tribunal) and related adjudication matters.

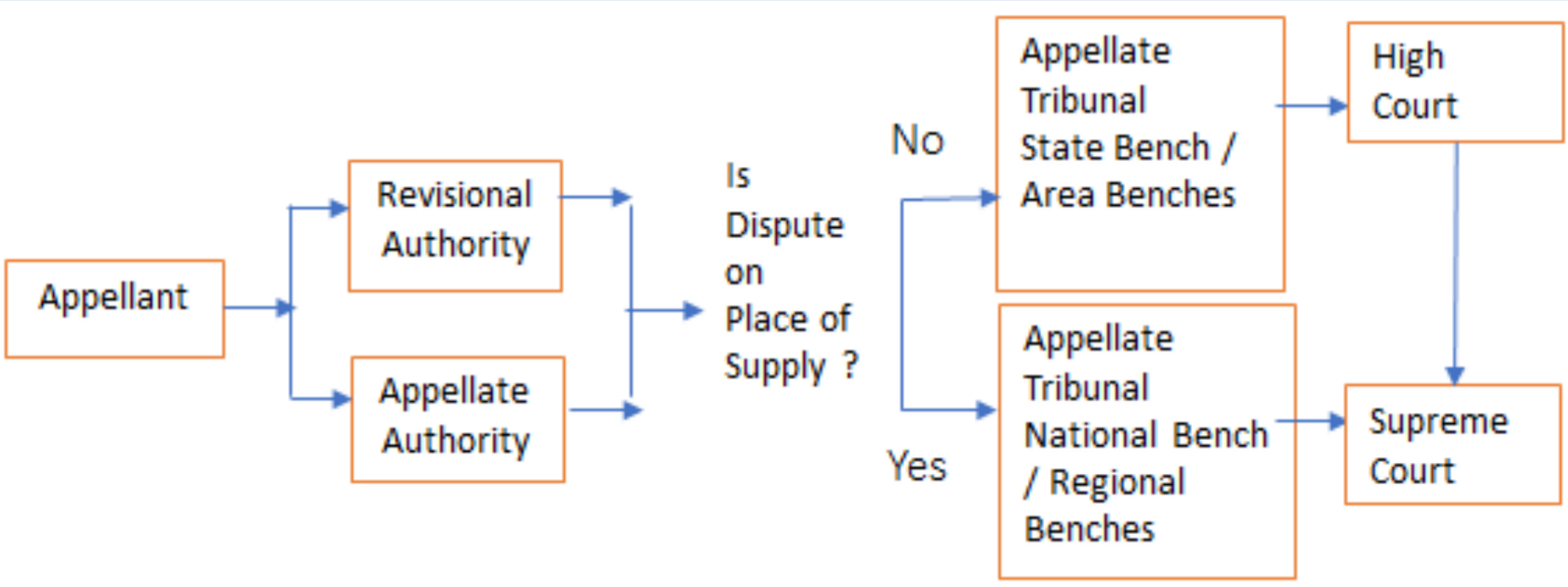

A) 4 Tier Appeal / Revision Framework :

Grounds of Appeal Given in GST Portal :

- Misclassification of any goods or services or both

- Wrong applicability of a notification issued under the provisions of this Act

- Incorrect determination of time and value of supply of goods or services or both

- Incorrect admissibility of input tax credit of tax paid or deemed to have been paid

- Incorrect determination of the liability to pay tax on any goods or services or both

- Whether applicant is required to be registered

- Whether any particular thing done by the applicant results in supply of goods or services or both

- Rejection of application for registration on incorrect ground

- Cancellation of registration for incorrect reasons

- Transfer/Initiation of recovery/ Special mode of recovery

- Tax wrongfully collected/Tax collected not paid to Government

- Determination of tax not paid or short paid

- Refund on wrong ground/Refund not granted/ Interest on delayed refund

- Fraud or wilful suppression of fact

- Anti profiteering related matter

- Others

B) REVISION BY Revisional Authority :

By-passing the Appellate Authority, tax payer aggrieved to a decision or order passed by adjudicating authority may approach to the Revisional Authority for remedy where there is no condition of pre-deposit. Notification no. 05/2020- Central Tax, dated 13th January2020, authorizes following officers as Revisional Authorities:

- Principal Commissioner or Commissioner of Central Tax for decisions or orders passed by the Additional or Joint Commissioner of Central Tax; and

- Additional or Joint Commissioner of Central Tax for decisions or orders passed by the Deputy Commissioner or Assistant Commissioner or Superintendent of Central Tax.

Erroneous and Prejudicial to the assessee :

- The order is Passed without making inquiries or verification which should have been made

- The order has not been made as per any order , direction or instruction issued by Board

- The order has not been passed as per any decision rendered by Jurisdictional High Court or Supreme Court in the case of tax payer or any other person

- Evidence in his possession that the tax payer has suppressed the taxable turnover

- Evidence in his possession that the tax payer has availed excessive ITC

Prejudicial to Revenue in following Cases :

- Supply has escaped levy thogh leviable

- Item has been taxed at low rate

- Wrong availment of ITC

- Wrong Utilisation of ITC

- Erroneous Refund